When it comes to managing business finances, one simple decision can have a big impact:

Should you use a business credit card or a debit card for expenses?

At first, both seem similar. They both allow you to pay for business purchases, track transactions, and manage spending. But when you look deeper — especially from an expense tracking and bookkeeping perspective — the differences become important.

If your goal is to improve small business expense management, the choice matters more than you think.

Expense tracking isn’t just about recording transactions — it’s about clarity.

The way you pay for expenses affects:

Choosing the right payment method helps you build a better business expense tracking system.

A business credit card allows you to spend first and pay later.

From a tracking perspective, this creates a clear, centralized record of all expenses over a billing cycle. Each transaction is logged, categorized, and grouped into a monthly statement.

This makes it easier to:

Credit cards also provide detailed transaction histories, which supports accurate bookkeeping for small business.

However, they require discipline. If balances are not managed properly, interest and fees can add up quickly.

A business debit card directly deducts money from your bank account.

This creates a real-time connection between spending and available cash, which can help with immediate cash flow management.

However, from a tracking perspective, debit cards can be slightly less structured. Transactions are recorded, but they may not always provide the same level of detail or categorization as credit card statements.

Also, since payments happen instantly, there’s less flexibility in managing short-term cash flow.

The core difference between a business credit card vs debit card comes down to how structured your financial data is.

Credit cards naturally organize expenses into billing cycles, making reviews easier and reports cleaner.

Debit cards keep spending simple and immediate, but may require more manual effort when analyzing expenses over time.

For businesses focused on scaling or improving financial clarity, structure often becomes more important than simplicity.

No matter which card you use, one thing doesn’t change:

👉 Transactions alone are not enough.

You still need:

Without these, your expense tracking system is incomplete.

Bank statements show that you spent money.

Receipts show why you spent it.

There’s no single answer — it depends on your business style.

A business credit card is often better if:

A debit card works well if:

Many businesses actually use both — combining control with flexibility.

Whether you use a credit card or debit card, the real challenge is organizing proof.

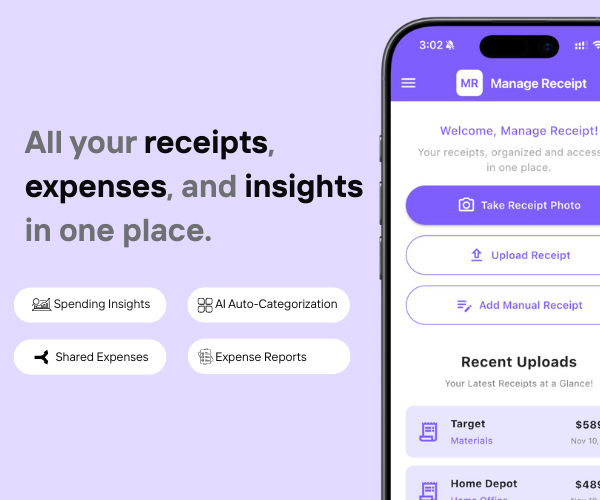

Manage Receipt helps bridge that gap by ensuring every transaction has proper documentation.

With Manage Receipt, you can:

Capture receipts instantly to prevent loss

Store all receipts in one centralized system

Access proof quickly for approvals and audits

Improve visibility into spending

Reduce manual work and admin overhead

This helps SMBs build a cleaner, faster, and more reliable expense process.

Click Here to know more about how Manage Receipt helps small businesses.

Choosing between a business credit card vs debit card isn’t just about payments — it’s about how effectively you can track and manage expenses.

Credit cards offer better structure and reporting. Debit cards offer simplicity and immediate control. But neither works well without proper systems.

When combined with tools like Manage Receipt, both options can become part of a reliable, organized, and efficient expense tracking system.

Because in business finance, it’s not just how you spend — it’s how well you track it.

From smartphones to air conditioners, big purchases come with big responsibilities. With Manage Receipt, you can stop worrying about lost receipt. Whether you’re requesting a refund or sending a product for repair, your receipts are always there when you need them.

© 2025 Manage Receipt. All Rights Reserved.